Planning a Fundraising Campaign

Plant growing on coins in glass jar. Increasing quantity of cash, startup, money growth concept

Startup Success: A Startup Fundraising Series

How Does a National Crisis Affect Startup Fundraising?

I have three adult daughters and two granddaughters. During the recent coronavirus outbreak, I worry most about their personal health safety. But I’m also worried about their personal financial security, and that causes me to think about the financial health of the companies they work for.

Startups are used to dealing with basic financial survival, but many that I talk to during these interesting times are more concerned than normal because they don’t know if their vehicles for funding their company are still available. The immediate impact to startups will be a slowdown and delay in funding activity while investors of most types try to decide for themselves how much worse things will get and how long the situation might last. The slowdown will also occur simply due to the increased difficulty of travel and recommended social distancing. Videoconferencing only goes so far when it comes to investor interactions.

Angel investors and family offices will be much more conservative as they deal with the value of their personal investment portfolio dropping quite a bit. However, after venture fund managers have a month or two to figure out how bad things might get, I’m of the belief they will continue to invest at a similar pace as before the crisis. That’s because a fund manager for a traditional 10-year fund needs to deploy their LP’s capital within the first three years (or so) of the fund to optimize their internal rate of return (IRR) and other key fund performance metrics. They can’t just sit on the sidelines for a year. The question is whether they’ll prioritize the use of their capital to help companies they invested in from their prior fund(s), thereby protecting their portfolio and potentially investing at a good valuation for the benefit of the LP’s in their current fund.

My opinion on venture funds would change quite a bit if the economy and stock market get so whacked that it causes fund LP’s to decommit on their capital calls, as happened in the years following the Great Recession. I’m also nervous about venture funds that have completed their initial close and started making investments, but haven’t yet reached their final close. Those funds will need to recalibrate their investing amounts and frequency.

The longer this “new normal” continues, the more the balance of negotiating power will increasingly swing to the investors’ favor. This translates to more aggressive and investor-friendly terms (we might start seeing 1.5–2.0x liquidation preferences and the like) and lower valuations. But I believe Silicon Valley valuations will take a far bigger hit than the middle of the country, where startups don’t typically experience wide ranges of increasing and decreasing valuation. Instead, their valuations tend to remain pretty steady throughout.

The previous Startup Success column focused on strategies for determining how much money to raise, while stressing the importance of funding desired outcomes rather than activities. Armed with these strategies, the startup is ready to plan out the phases of a fundraising campaign.

A successful fundraising campaign always has a rhythm, no matter the stage of the company. It has a start, a middle, and an end. It is critical to plan that rhythm and understand the associated time commitment before launching the campaign. Entrepreneurs are taught to move fast and break things, but doing so with a fundraising campaign will actually deliver on the stated promise: It will break things.

Allocating Time and Priority

Maintaining the proper rhythm throughout a fundraising campaign involves careful allocation of both time and priority. Most entrepreneurs know things won’t play out exactly according to the plan, but having a plan helps them figure out when it’s time to adapt on the fly.

Before Starting: Pick a Team Captain

During the pre-seed and seed stages of funding, it might be obvious who will lead the fundraising efforts, but that might be because there is only one full-time member of the team. If, instead, there are multiple cofounders but no one individual carries the CEO title (versus just “founder”), only one person should bear the burden of being the fundraising lead. Trying to share the duty will be as ineffective as rotating sales reps each week for a million-dollar opportunity with a large enterprise, or rotating football quarterbacks with each play. The fundraiser needs to get into a rhythm, which means context switching isn’t helpful.

This doesn’t mean investors won’t want to meet and interact with other members of the team; they will. But the chief fundraiser leads the process and is the frontline person for most interactions. Once a founder adopts the title of CEO, she will become the chief fundraiser by default. Being the CEO and serving as the chief fundraiser go hand in hand throughout the life of the company. Investors want to evaluate and get to know the CEO more than any other member of the team.

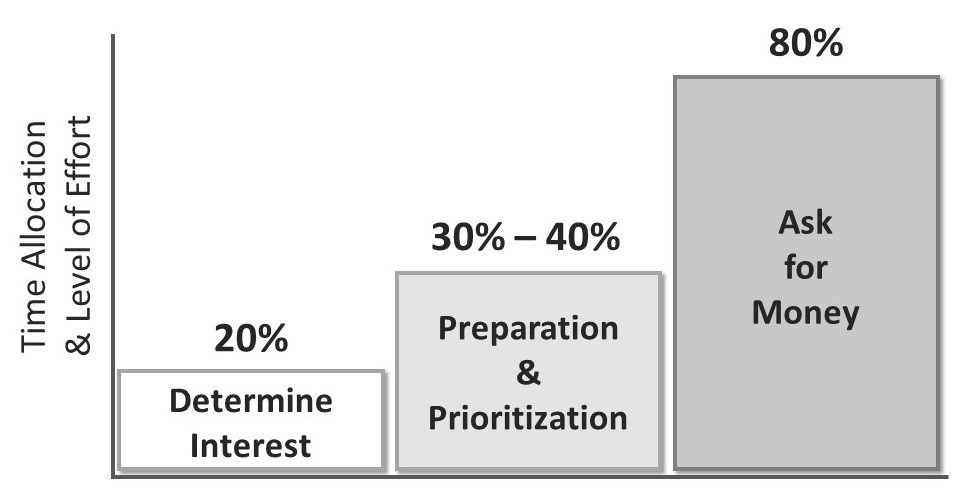

Start: Determine Investor Interest

The purpose of the first phase is relationship building. While it’s going on, it should consume about 20 percent of the fundraiser’s time. Over the course of a month or two, they should try to determine which investors could be viable prospects, and that is best accomplished by meeting with them before actually being ready to hit them up for investment. In fact, they should make that clear when reaching out to them by saying something like “We’re not raising money at the moment, but I wanted to see if I could spend some time with you to let you know what we’re working on and to get your feedback.”

With the understanding that the fundraiser isn’t going to ask them to write a check at the end of the meeting, investors will give some of the most honest feedback possible. Their questions, concerns, level of excitement, body language, and—hopefully—a twinkle in their eye will inform the fundraiser as to their level of interest. The reactions fundraisers get across these meetings (and you might have dozens of such meetings) should be analyzed carefully before the next phase.

Even when not executing a fundraising campaign, startups should always operate in some level of relationship building. The most successful startups I work with are perpetually fundraising, which means that, even when they aren’t actively executing a campaign, they’re building and grooming their investor pipeline for the next round.

Middle: Preparation and Prioritization

The purpose of this phase is to take the campaign on a test-drive while setting the environment for the final phase, in which they will actually hit up potential investors for money. Over the course of several weeks, the fundraiser should interact with the most interested investors from the first phase to get the next level of feedback. If a company is raising a small round and has fewer than 10 interested investors, this middle phase might only take a couple of weeks. For a larger round that includes interested institutional investors, it could take a month or more.

This phase should consume 30 to 40 percent of the fundraiser’s time. For startups raising funding out of need instead of want, the stakes get higher during this phase. Stress increases because, by now, the startup is definitely watching the projected date on which they will run out of cash.

These interactions with investors will be more specific than in the starting phase. The fundraiser is now exposing investors to the amount of money the company has decided to raise, the proposed terms, and the milestones expected to be reached with new funds. In some cases, the fundraiser will communicate ranges, to gauge investor reaction and not lock themselves into a given number. If the fundraiser completes this phase correctly, by the end they will have a list of investors (prioritized by likelihood of investment), a specific amount to raise, and a final set of proposed terms.

End: Ask for Money

Too many startups begin their campaign by hitting up investors for funds while adjusting their proposed terms along the way. Not only is this inefficient, but it burns bridges. It’s not very effective to come back to an investor after a failed pitch to inform them that the terms are now more attractive. For something as important as a fundraising campaign, it’s best to measure twice and cut once.

The end phase should consume at least 80 percent of the chief fundraiser’s time. That means the cofounders and other team members have to pick up her workload. Let me be really clear on this: Fundraisers cannot dial in this phase at only 50 percent of their time. If they execute the prior phases effectively and are representing a sound investment opportunity, they should have created momentum they can capitalize on aggressively. That means the business won’t advance at the same pace as before, and this is another reason to get aggressive on closing the funding round.

Identifying Prospective Investors

Now that we understand the key phases of the campaign from start to finish, we can examine the process of identifying prospective investors. Much like a marketing campaign that has an objective of securing new customers, the fundraising campaign could be diagrammed as a funnel. The fundraiser must start by filling the top of the funnel with prospective investors. If they can’t find them, they can’t build a relationship with them. And just like a marketing campaign, the quality of the prospects makes a big difference in the efficiency and effectiveness of the campaign. Optimizing the mix investor prospects, and balancing quality and quantity, takes a lot of research and a lot of hustle.

Ideal Targets by Stage

Most investors are stage-specific. In other words, they only invest in seed-stage companies or only in Series A companies. So, let’s start by looking at the most common types of investors by funding stage.

Pre-Seed

Friends and family are the most likely source of investment before the product is launched and before revenue is being generated. However, startups shouldn’t just take investments from anyone willing to support them; in many cases, they must be accredited investors as defined by the US Securities and Exchange Commission (SEC). Crowdfunding portals can be a good solution for some startups that haven’t launched their product, but research is needed to compare the options and to make sure the product is a good candidate for presales via crowdfunding. Government grants are also a possibility, and research is needed to find the right programs. Angel investors are yet another possibility, but only a very small subset of angels will participate in a pre-seed round—and they aren’t easy to find.

Seed

Angel investors are the dominant source of investment for the seed stage. They can invest solo or as part of an angel network or syndicate. Angels that invest solo usually only do so in their areas of expertise, which usually means startup ventures that somehow overlap with their own professional career. Their online biography or LinkedIn profile can serve as a good source of information for filtering and rating them. There are also some venture funds that invest in seed-stage startups, although they are in the minority.

Series A

Venture funds are the dominant source of investment for Series A funding. They usually have one or more areas of focus, dictated by their investment strategy. This can be along industry lines (healthcare, education, real estate), technologies (artificial intelligence, virtual reality, robotics), business models (ecommerce, marketplaces, tech licensing), solution types (mobile apps, SaaS, hardware), customer segments (consumer, small- to medium-size businesses [SMB], enterprise, government), or just about any aspect of a business plan you can think of. The good news is that venture funds make it easy to decode their investment strategy; the fundraiser can just read their website and look at their existing portfolio of investments.

Regardless of the funding stage, the fundraiser’s mission is to find the right investors to meet with rather than just seeking out anyone who invests in startups. This requires research on each prospect, and prioritizing based on how aligned their investment strategy is with the business.

Where to Find Investors

Venture funds, angel networks, crowdfunding portals, and government grant programs are all searchable online. Success in finding the best targets is mostly a matter of effort. Individual angel investors are much more difficult to find, at least the best ones for a specific startup. That’s because they don’t have websites and don’t openly published investment criteria. In fact, they aren’t always actively investing, so even if the fundraiser discovers a perfect match, the investor might not be investing at the time the startup needs the money.

To find the best angels, fundraisers have to go where they hang out. Some are members of angel networks or similar angel-investing syndicates. And even though they sometimes invest with a group, many of them invest individually as well. Some are affiliated with startup incubators and accelerator programs, probably as a mentor or maybe in a leadership role. Some serve as a judge for pitching events and hackathons. Getting involved with those groups and activities is a good way to meet angel investors.

For those who live in a city that doesn’t have much in the way of angel networks, startup accelerators, startup-pitching events, and the like, it’s going to be a lot more difficult. Angel investors very much like to invest locally so they can keep tabs on their investments while actively helping their portfolio of startups as an advisor of sorts. This means that angels from elsewhere in the state or a neighboring state might still be candidates, but securing an investment from them is going to be more difficult.

***

As we have seen, successful fundraising campaigns have a certain rhythm. Time spent planning out this campaign rhythm and identifying the best targets will pay dividends, improving the odds of raising the desired amount from the right investors. But if the startup begins randomly pitching investors without preparation, they risk losing credibility and wasting time. Since credibility with prospective investors is absolutely required and time is a startup’s most valuable resource, such lack of planning is a double whammy. I would rather see a fundraiser tell an interested prospective investor they haven’t yet launched their round of funding rather than try to formally pitch the investor unprepared.

A fundraising campaign almost always involves a lot more time and effort than anticipated. Fundraisers should mentally prepare to grind through lots of meetings and lots of rejection. But they should also know that each positive meeting recharges the battery. Those boosts—combined with the fire they already have in their belly—will propel them through the fundraising grind.